Retirement planning is one of the most important financial goals in life. Many people believe that creating a retirement corpus worth crore requires a very high income or large investments. However, the power of disciplined investing, compounding, and time can help even small monthly investments grow into a substantial retirement fund. A monthly SIP (Systematic Investment Plan) of just ₹5,000 can potentially help you build a retirement corpus of around ₹3.5 crore if you start early and remain invested for the long term.

Why Retirement Planning Matters

As life expectancy increases, retirement periods are becoming longer. Today, a person retiring at 60 may easily live another 25–30 years. During this period, regular salary income stops, but expenses continue. Medical costs, inflation, lifestyle expenses, and emergencies can significantly impact financial security.

Without proper retirement planning, maintaining the desired lifestyle after retirement can become challenging. Therefore, starting early and investing consistently is essential.

Understanding the Power of Compounding

Albert Einstein reportedly called compounding the eighth wonder of the world. Compounding means earning returns not only on your original investment but also on the returns generated over time.

When you invest regularly through SIPs, your money gets more time to grow. The earlier you start, the greater the benefit of compounding.

For example:

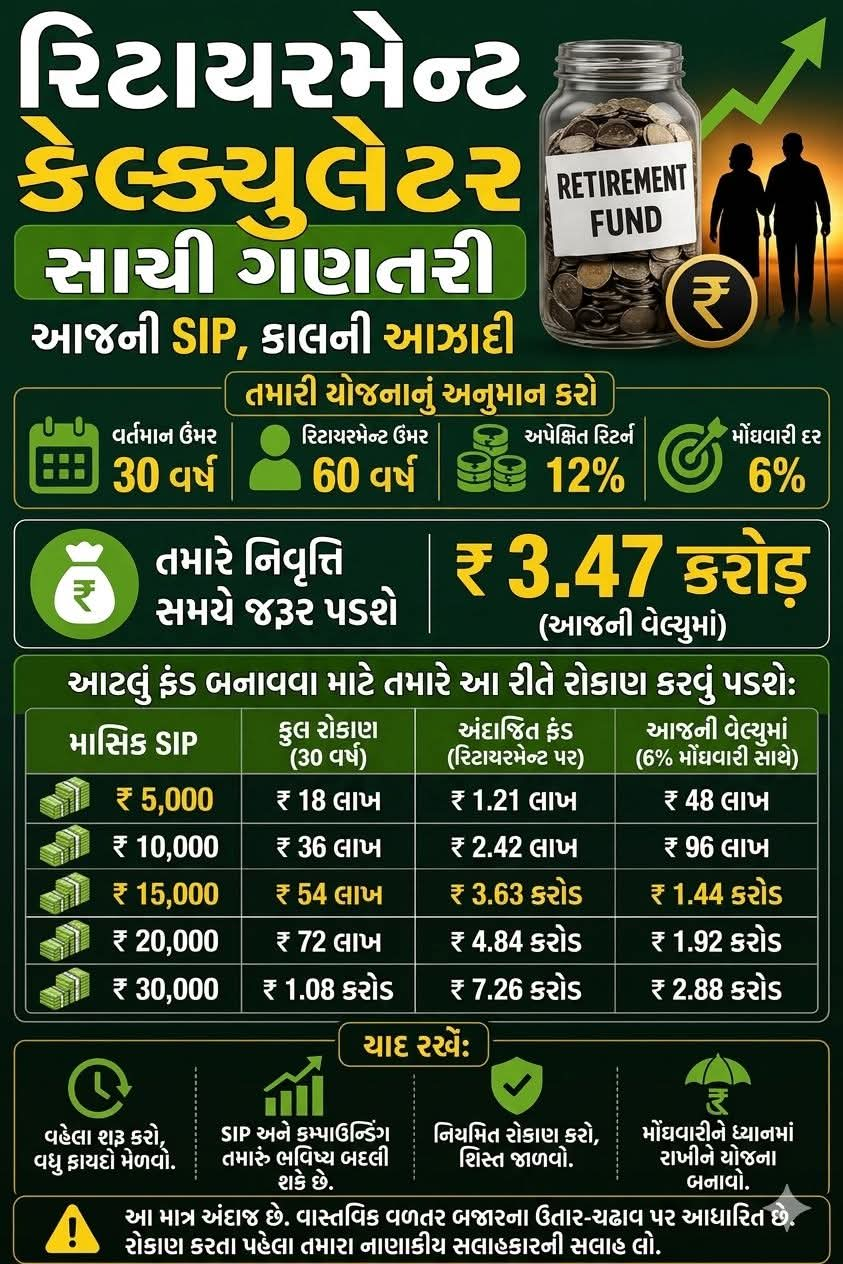

- Current Age: 30 Years

- Retirement Age: 60 Years

- Investment Duration: 30 Years

- Monthly SIP: ₹5,000

- Expected Annual Return: 12%

Under these assumptions, your investment can grow significantly over the next three decades.

Retirement Corpus Calculation

Let us understand the numbers:

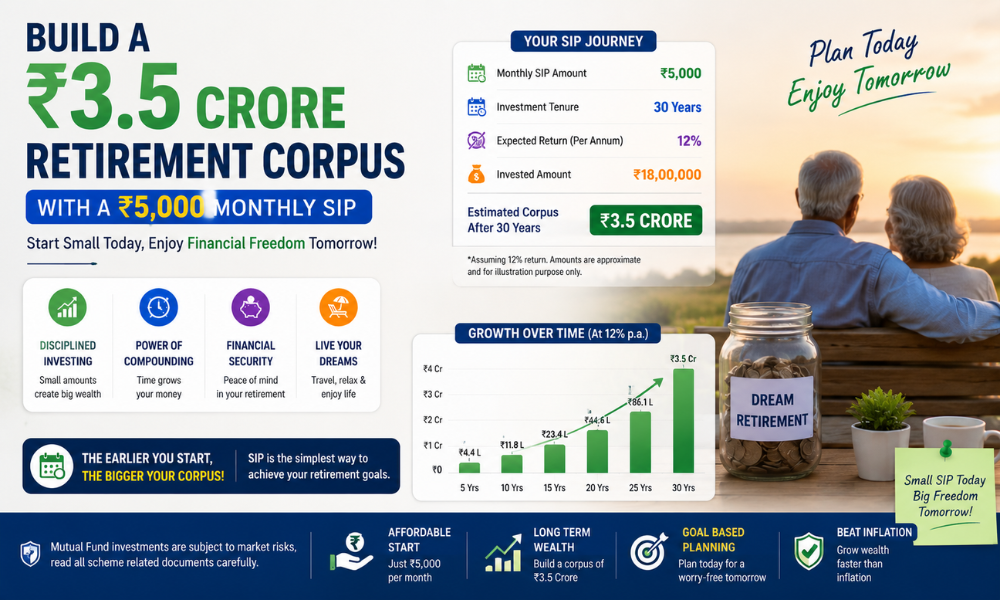

Monthly SIP: ₹5,000

- Total Monthly Investment: ₹5,000

- Investment Period: 30 Years

- Total Amount Invested: ₹18,00,000

- Estimated Value at Retirement (12% Return): Around ₹1.76 Crore

However, retirement planning should also consider inflation. Assuming inflation averages around 6% annually, the future value required to maintain today’s purchasing power may be approximately ₹3.47 Crore at retirement.

This means that the retirement corpus you build today should be capable of supporting your lifestyle despite rising costs in the future.

How Inflation Affects Retirement

Inflation silently reduces the purchasing power of money.

For example:

- A product costing ₹100 today may cost around ₹574 after 30 years at 6% inflation.

- Healthcare expenses generally rise even faster than average inflation.

- Daily living expenses, travel, utilities, and leisure activities also become more expensive over time.

Therefore, retirement planning should always account for inflation rather than focusing only on the investment amount.

SIP Scenarios for Retirement Planning

The following examples show how different SIP amounts may grow over 30 years at an estimated 12% annual return:

SIP of ₹5,000 Per Month

- Total Investment: ₹18 Lakh

- Estimated Retirement Corpus: ₹1.76 Crore

- Inflation-Adjusted Future Requirement: ₹3.47 Crore

SIP of ₹10,000 Per Month

- Total Investment: ₹36 Lakh

- Estimated Retirement Corpus: ₹3.52 Crore

SIP of ₹15,000 Per Month

- Total Investment: ₹54 Lakh

- Estimated Retirement Corpus: ₹5.28 Crore

SIP of ₹20,000 Per Month

- Total Investment: ₹72 Lakh

- Estimated Retirement Corpus: ₹7.04 Crore

SIP of ₹30,000 Per Month

- Total Investment: ₹1.08 Crore

- Estimated Retirement Corpus: Over ₹10 Crore

These examples demonstrate how increasing your SIP amount can dramatically impact your retirement wealth.

Benefits of Starting Early

Starting early offers two major advantages:

- Longer Compounding Period

A person starting at age 30 gets 30 years of compounding before retirement. Someone starting at age 40 gets only 20 years.

Even if the later investor contributes more money, they may struggle to match the wealth accumulated by the early investor.

- Lower Monthly Investment Requirement

The earlier you begin, the smaller the monthly investment needed to achieve your target corpus.

Waiting even five years can significantly increase the SIP amount required to reach the same goal.

Strategies to Reach Your Retirement Goal Faster

Increase SIP Regularly

Instead of investing the same amount every year, increase your SIP whenever your income increases.

A 10% annual SIP step-up can substantially boost your retirement corpus.

Stay Invested During Market Volatility

Market fluctuations are normal. Long-term investors should avoid panic selling during market corrections.

SIPs benefit from market volatility through rupee cost averaging, which helps accumulate more units when prices are lower.

Diversify Investments

A diversified portfolio may include:

- Equity Mutual Funds

- Index Funds

- Hybrid Funds

- Debt Funds

- Emergency Fund

Diversification helps manage risk while maintaining growth potential.

Review Your Retirement Plan Annually

Life circumstances change over time. Review your retirement goals, inflation assumptions, and SIP contributions at least once a year.

Common Retirement Planning Mistakes

Avoid these common errors:

- Delaying investments until later in life

- Ignoring inflation

- Withdrawing investments frequently

- Stopping SIPs during market downturns

- Depending entirely on savings accounts or fixed deposits

- Not reviewing financial goals periodically

Key Takeaways

- Start retirement planning as early as possible.

- Even a ₹5,000 monthly SIP can create substantial wealth over the long term.

- Compounding works best when given enough time.

- Inflation must be considered while calculating retirement requirements.

- Increasing SIP contributions regularly can significantly enhance retirement wealth.

- Consistency and patience are often more important than investing large amounts.

Conclusion

Building a retirement corpus of approximately ₹3.5 crore may seem like a daunting task today, but it becomes achievable when approached systematically. A disciplined SIP of ₹5,000 per month, combined with long-term investing, compounding, and periodic increases in contributions, can help create significant wealth for retirement.

The most important step is not finding the perfect investment but starting early and remaining consistent. Every year you delay retirement planning reduces the power of compounding and increases the investment required later. Begin today, stay invested, and allow time and compounding to work in your favor toward a financially secure and comfortable retirement.